One lawsuit, one natural disaster, one data breach — and an uninsured small business can be financially destroyed overnight. Business insurance is not a luxury or a bureaucratic formality. It's the single most important financial protection you can put in place for the business you've worked so hard to build.

The challenge for most small business owners is that the insurance market is confusing, filled with overlapping policy types and aggressive salespeople. This guide cuts through the noise and tells you exactly which types of insurance your business actually needs (and which are worth skipping), how much you should be paying, and where to get the best coverage for your situation.

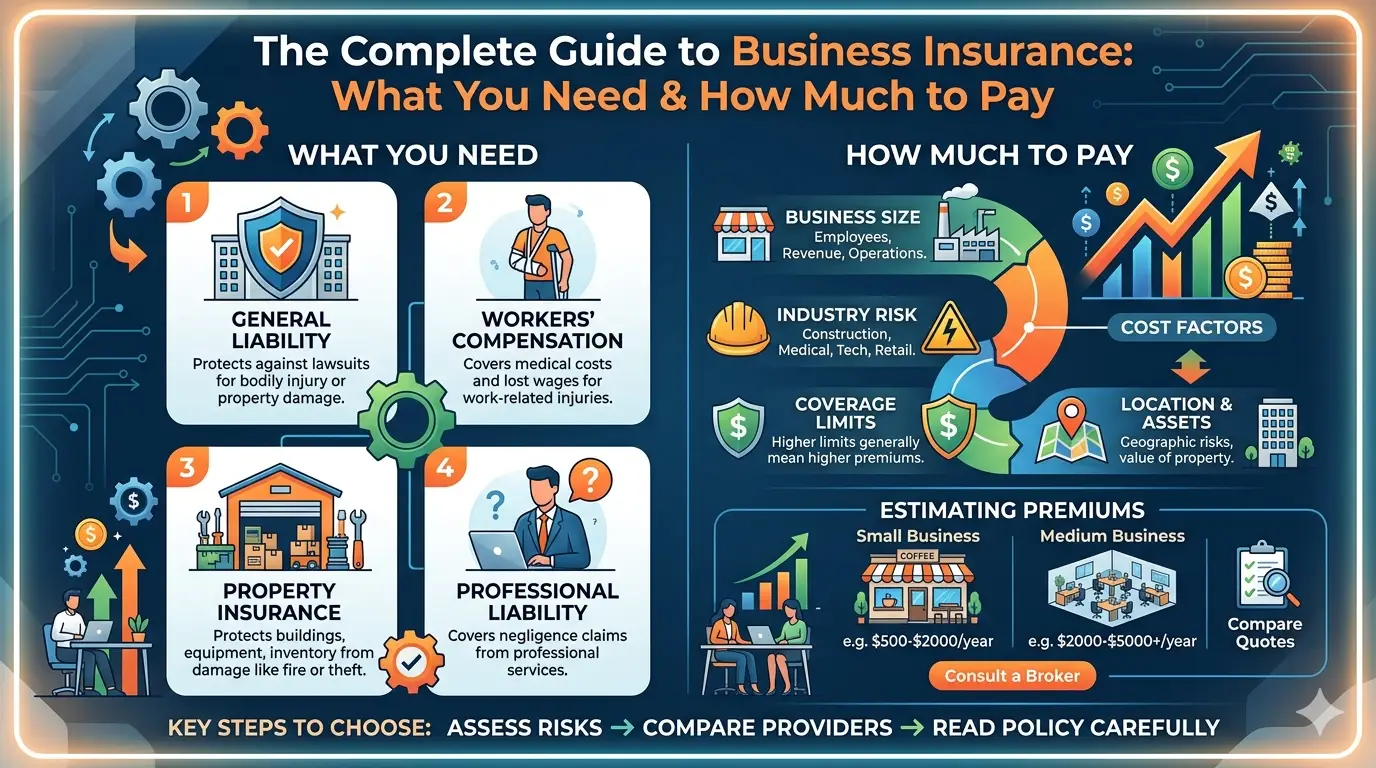

The 7 Core Types of Business Insurance

1. General Liability Insurance (GLI)

⚠️ Required for MostGeneral liability insurance protects your business from third-party claims of bodily injury, property damage, and personal injury (like libel or slander). If a customer slips on your floor, if your employee accidentally damages a client's property, or if someone sues you claiming your advertising harmed their business — GLI covers legal defense costs and settlements.

Who needs it: Almost every business. Many landlords require it before leasing space; clients often require a Certificate of Insurance before signing contracts.

2. Professional Liability (Errors & Omissions)

⚠️ Essential for Service BusinessesProfessional liability — also called Errors & Omissions (E&O) insurance — protects you if a client claims your work caused them financial harm due to errors, omissions, or negligence. A consultant who gives advice that loses a client money, an accountant who makes a tax filing mistake, a web designer whose code causes data loss — these scenarios are exactly what E&O covers.

Who needs it: Consultants, accountants, lawyers, architects, engineers, IT professionals, real estate agents, financial advisors, marketers, and any professional who provides advice or services for a fee.

3. Business Owner's Policy (BOP)

✅ Recommended for Most Small BusinessesA Business Owner's Policy bundles General Liability and Commercial Property insurance into a single, discounted package. It's designed specifically for small businesses (typically under $5M revenue) and costs 15–25% less than buying the policies separately. A BOP covers both liability claims and physical assets (equipment, inventory, furniture, and the business itself).

If you have a physical location or significant business assets, a BOP is typically the best value for comprehensive basic coverage.

4. Workers' Compensation Insurance

⚠️ Required in Most StatesIf you have employees, workers' comp is legally required in 49 out of 50 U.S. states (Texas is the exception). It covers medical expenses and lost wages for employees injured on the job, and protects you from employee lawsuits related to workplace injuries. The cost varies significantly by industry — a desk job business pays far less than a construction company.

5. Cyber Liability Insurance

✅ Increasingly EssentialCyberattacks on small businesses increased by 300% between 2019 and 2024. If your business stores customer data, processes online payments, or relies on digital systems (which is almost every business in 2026), cyber liability insurance covers the costs of a data breach: notification costs, credit monitoring for affected customers, legal fees, regulatory fines, and business interruption losses.

The average cost of a small business data breach is $200,000 — enough to bankrupt most SMBs without insurance.

6. Commercial Auto Insurance

⚠️ Required if Using Vehicles for BusinessIf you or your employees use vehicles for business purposes — making deliveries, visiting clients, transporting equipment — personal auto insurance does NOT cover accidents that occur while conducting business. Commercial auto insurance covers vehicles used for business with appropriate liability limits. Note: rideshare apps and food delivery platforms have their own requirements.

7. Business Interruption Insurance

✅ Highly Recommended Post-COVIDBusiness interruption insurance replaces lost revenue when your business is forced to close due to a covered event — fire, natural disaster, or other physical damage. It covers ongoing expenses (rent, payroll, loan payments) during the closure period. The COVID-19 pandemic taught many small business owners the painful lesson that without this coverage, a forced closure can permanently end a business.

Insurance Costs by Business Type

| Business Type | Minimum Coverage Needed | Estimated Annual Cost | Priority Coverage |

|---|---|---|---|

| Freelancer / Consultant | E&O + GLI | $800–$2,500/year | Professional Liability |

| Retail Store | BOP + Workers' Comp | $1,500–$4,000/year | BOP (property + liability) |

| Restaurant / Food Service | BOP + Workers' Comp + Liquor Liability | $3,000–$10,000/year | Workers' Comp + Liability |

| Construction / Trades | GLI + Workers' Comp + Commercial Auto | $5,000–$15,000/year | Workers' Comp (high risk) |

| Tech / SaaS Company | Cyber + E&O + GLI | $2,000–$6,000/year | Cyber Liability |

| E-commerce | Product Liability + Cyber + BOP | $1,500–$4,000/year | Product Liability |

| Real Estate Agent | E&O + GLI | $1,200–$3,500/year | E&O (mandatory in most states) |

5 Ways to Lower Your Business Insurance Costs

- Bundle policies: A Business Owner's Policy (BOP) bundles GL + Commercial Property at 15–25% discount vs. buying separately.

- Increase your deductible: Raising your deductible from $500 to $2,000 can lower premiums by 15–20%. Only do this if you have adequate cash reserves to cover the deductible.

- Pay annually: Most insurers charge a 3–8% fee for monthly payment plans. Paying annually eliminates this.

- Improve risk management: Installing security systems, training employees on safety, and implementing cybersecurity protocols can qualify you for lower-risk pricing tiers.

- Shop every 2–3 years: Insurance is a competitive market. Getting 3+ quotes at renewal can often reduce your premium by 10–20% without reducing coverage.

Insurance You Probably Don't Need (Yet)

Insurance salespeople will try to sell you everything. Here's what most small businesses can defer until they're larger:

- Key Man Insurance: Only relevant if your business has multiple partners or investors. Skip until you're generating $500K+ revenue.

- Employment Practices Liability (EPLI): Covers wrongful termination/discrimination suits. Important once you have 10+ employees.

- Directors & Officers (D&O) Insurance: Protects board members. Only relevant if you have investors or a formal board.

- Umbrella Insurance (above $2M): Useful once you have significant assets to protect. Most small businesses don't need more than $2M in liability coverage initially.

Where to Get Business Insurance in 2026

For most small businesses, the fastest and most cost-effective way to get coverage is through an online business insurance marketplace. These platforms let you compare quotes from multiple insurers in minutes:

- Next Insurance — 100% online, certificates in minutes, excellent for freelancers and contractors. Average BOP from $25/month.

- Hiscox — Strong for professional services, tech, and consulting. Competitive E&O pricing.

- The Hartford — Best for established businesses needing complex coverage. Excellent claims service reputation.

- Chubb — Premium option for businesses with higher revenues and more complex risk profiles.

For complex situations — multiple locations, high-risk industries, significant revenue — work with an independent insurance broker who can access policies from many insurers and provide expert guidance on coverage structure. This typically costs no more than buying direct.

Conclusion: Protect What You've Built

Business insurance is not glamorous, but it's foundational. A single uninsured incident can wipe out years of hard work, savings, and sacrifice. The right coverage — purchased intelligently, structured correctly, and reviewed annually — is one of the most important investments you can make in the long-term sustainability of your business.

Start with the essentials: GLI or a BOP for most businesses, E&O if you provide professional services, and Workers' Comp the moment you hire your first employee. Add Cyber Liability if you handle customer data. Review your coverage annually as your business grows.

For more on financial protection and business planning, read our guides on cash flow management, business funding options, and personal finance for entrepreneurs.

🔗 Related Resources

Written and reviewed by

Rachel Torres

Rachel Torres is the BusinessFocusHub editorial author for practical guides on business finance, marketing, productivity, and online tools. Her articles focus on clear steps, realistic trade-offs, and reader-first advice for entrepreneurs and small business owners.